-

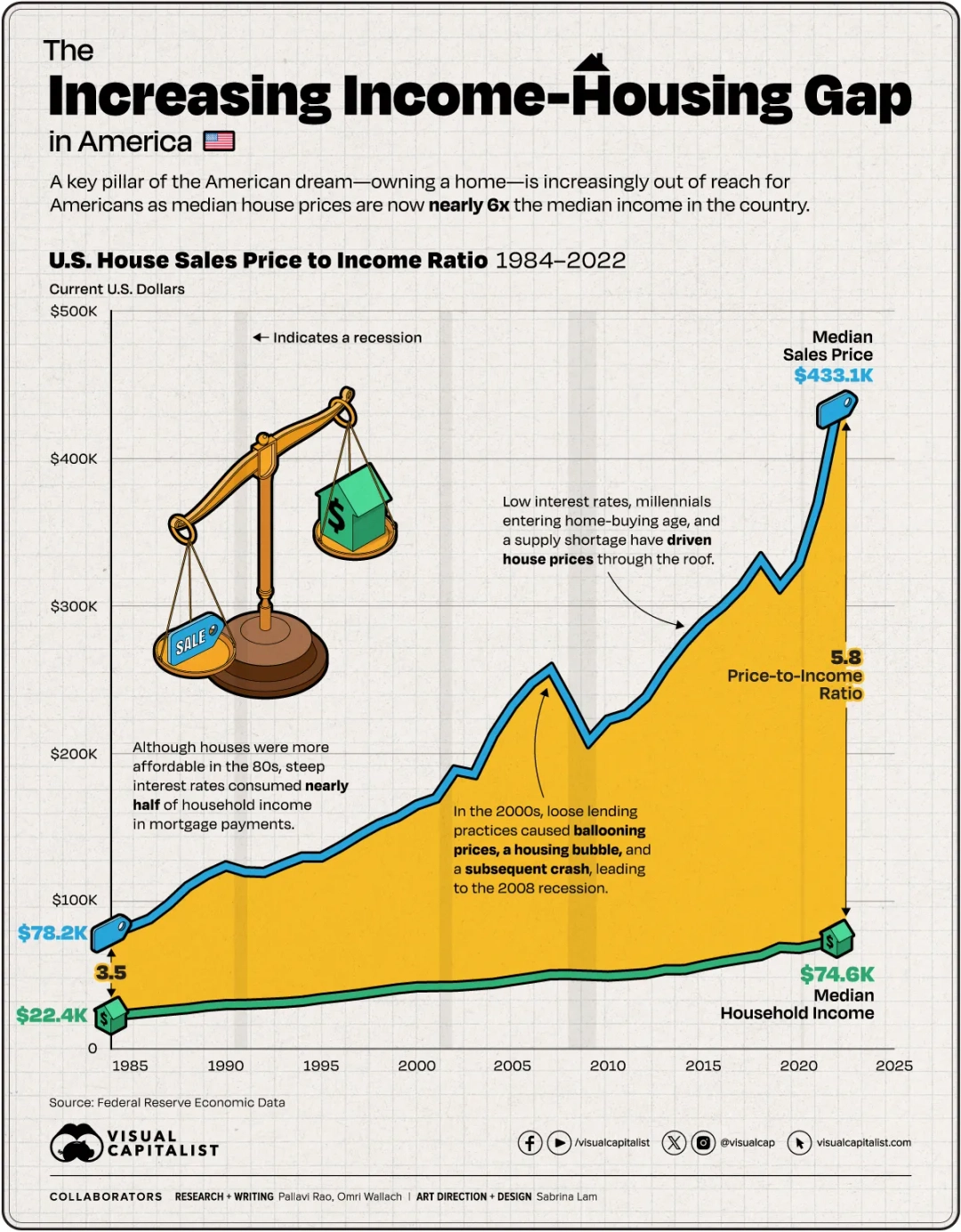

A Housing Crisis In America

There are a lot of different ways to look at the current housing situation in the US. I think the chart below best describes the challenges we are facing today and moving forward.

A Few Things To Consider

Current Homeowner Equity: 65% of American households are currently homeowners. Most current homeowners have large amounts of equity so selling their home would include a huge windfall that can be carried into their next home but what about the next generation?

Interest Rates: Mortgage interest rates follow the 10 year treasury bond which is expected to continue to increase over the next 5 years.

What About New Construction?

What Is ACTUALLY being built? I ran the numbers through the MLS looking at all the new construction homes sold over the past 6 months in PG, Anne Arundel, and all of SOMD. There were 406 detached homes sold with an average sales price of $743,613!!!

For townhomes and condos there were 916 homes sold and the average sales price was $515,288

Let’s do a quick exercise on the average new construction home in Maryland as a first time homebuyer assuming you did not sell a home so you are using FHA requiring 3.5% down. (Don’t forget you need about another 32k for closing costs!)

(The Average New Construction Single Family Home In Maryland 2024/25)

-

Home Price: $743,000

-

Down Payment: 3.5% (minimum for FHA) = $26,005

-

Loan Amount: $743,000 – $26,005 = $716,995

-

Interest Rate: 7% (as of January 2025)

-

Loan Term: 30 year fixed rate

-

Annual Property Taxes: 1% of home value = $7,430

-

Annual Homeowner’s Insurance: $3,100

Calculations:

-

Monthly Property Taxes: $7,430 / 12 = $619.17

-

Monthly Homeowner’s Insurance: $3,100 / 12 = $258.33

-

Estimated Monthly Mortgage Payment (Principal & Interest): Around $4,780 (this can be more accurately determined with a mortgage calculator using the loan amount, interest rate, and loan term)

-

Total Monthly Payment: $4,780 (principal & interest) + $619.17 (property taxes) + $258.33 (insurance) = $5,657.50 👀

-

Maximum Allowable DTI: 43% is a common maximum for FHA loans.

-

Required Monthly Income: $5,657.50 / 0.43 = $13,157

-

Required Annual Income: $13,157 x 12 = $157,884

Therefore, to afford a $743,000 home with an FHA loan, considering the provided property taxes and insurance, you would need an (minimal) estimated annual income of approximately $157,884. (that’s with no other debt!)

My Thoughts

The reality of our current situation is that most homeowners are fine because they are sitting on trillions in equity. The upcoming generation is being forced out of the market and will have to either rent or buy a townhouse.

Silver Lining?

I think it is important to consider that while it’s clear the next generation will not realize the American Dream in the same way as their parents and grandparents did, we are still thriving if you look back just a little further.

Housing, the work environment, modern transportation, and modern healthcare are all infinitely better compared to 100 years ago. The working poor in America live better than kings 500 years ago.

We live in America and there is currently an optimism about the future. Recent polls show that for the first time in a long time, most Americans are optimistic about the future.

My advice to first time homebuyers is the same as what I told my daughter and son-in-law who purchased a home last year. Buy a home with income producing capability to cover the higher cost or buy a fixer upper and start building equity.

The fact of the matter is owning a home is still the #1 way for Americans to build wealth and long term financial security, that hasn’t changed. Thank you for coming to my Ted Talk!

-